Our mission at Sidekick is to help people meaningfully grow their wealth over the long term. To do this, as discussed in our previous article ‘How we Invest’, we’re focusing on unlocking opportunities traditionally reserved for only the wealthiest investors and are building an investment proposition around three key pillars:

- Expertly managed portfolios

- Access to modern alternative assets

- An open and engaging investor experience

But, access to return-generating investment products is only half of the solution…

Customers still need to remain long-term invested: it’s the compounding effects of the investment returns that make the real difference. As the chart below shows, over a 30 year period, staying invested in global equities versus having cash in a MoneyMarket fund could have delivered 3x the returns.

Markets are volatile and investments can have good and bad years, so having a long-term outlook and staying invested remains key to riding out the bumps and maximising gains. To quote Charlie Munger: “The first rule of compounding: Never interrupt it unnecessarily”.

But all too often, retail investors miss out on the benefits of long-term compounding.

We suffer from behavioural biases: we trade too frequently, we’re prone to selling when the markets drop, and we take gains when there is even more growth to be had.

And we’re often forced sellers: life can take unexpected turns and there can be unplanned expenses (such as home improvement costs or a tax bill), which mean we need access to cash and have to sell our investments. This is a personal problem I’ve experienced a number of times as an entrepreneur who’s had to fund the early days of a startup with little to no salary.

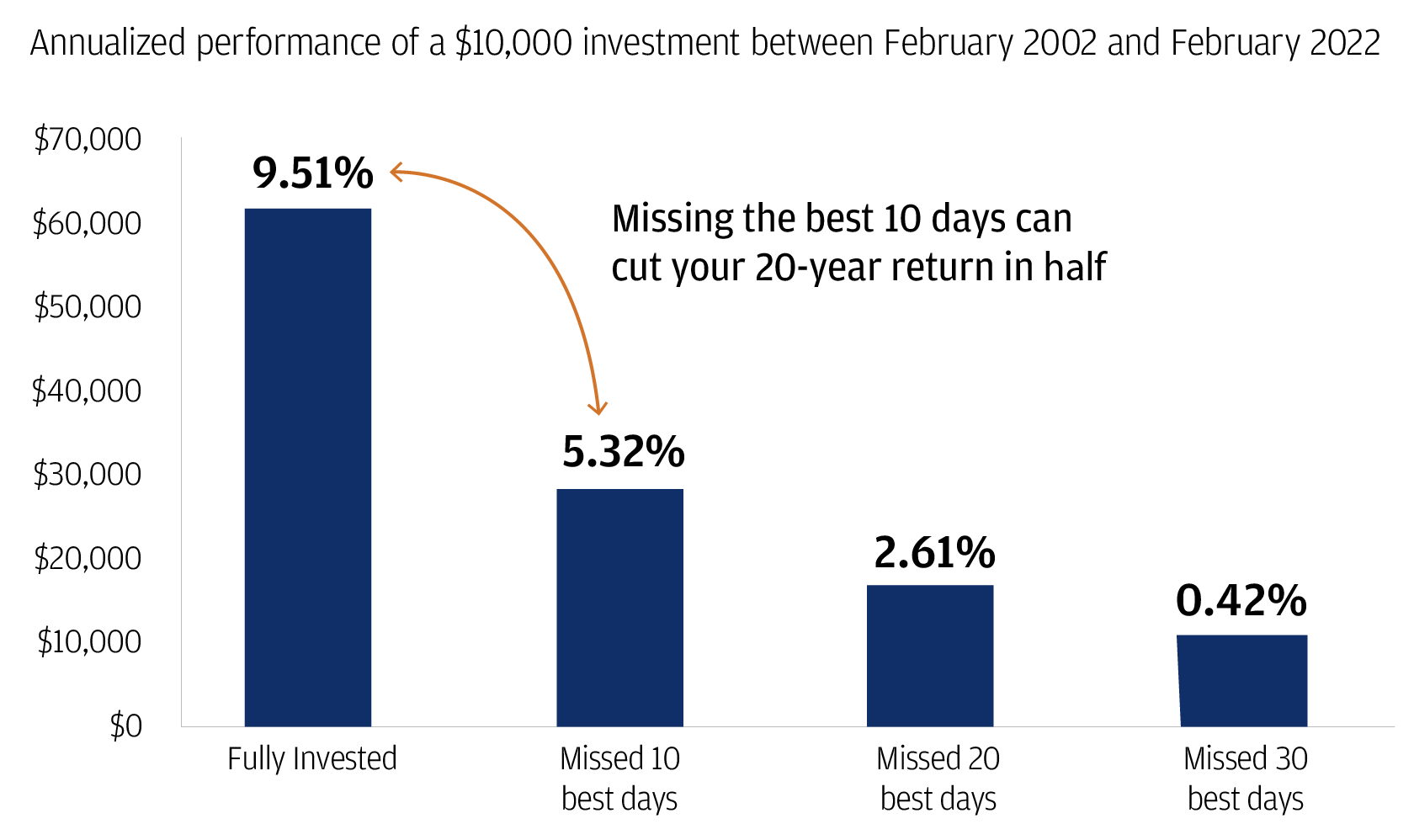

All too often, long-term goals are compromised by short-term actions and it can have huge implications on investment returns. As analysis from JP Morgan[1] shows, missing just 10 of the best days over a 20 year period can cut your returns in half!

The liquidity of investments is a double-edged sword.

"Liquidity is the ease and speed at which an asset can be bought or sold in the market."

On one hand, liquidity in investments is of great benefit as it helps provide financial agility and a safety net for unexpected cash needs. On the other hand, though, the ease and temptation to sell investments in response to market fluctuations can negatively impact long-term returns, creating a "liquidity paradox" where the availability of liquidity can be detrimental to achieving maximum returns.

The balance between liquidity and illiquidity is an area where wealthier investors also have significant advantages. They can often afford to lock up more of their money for longer (in vehicles such as hedge funds, private equity etc). And if they’re customers of private banks, they’re also likely to have access to flexible low cost credit, secured against their investment portfolios, when they need it.

The short-term liquidity versus long term returns conundrum is often a solved problem for high-net worths: they can have both… A way to access cash when you need it, without sacrificing their long-term investments: it’s sometimes known as a portfolio line of credit.

But the rest of us don’t have those opportunities, and we at Sidekick don’t think that’s fair. So that’s why we’ve developed our own Sidekick portfolio line of credit product, designed from the ground up for the retail customer. This product unlocks new opportunities for a wider set of customers, and helps level the playing field further.

“The last remaining fintech frontier”

…That’s how one of our research interviewees described it.

Democratisation of access has occurred across so many fintech verticals and products, but the ability to utilise your assets and borrow at low rates against them is still largely the privilege of the wealthiest.

- Stay invested for the long term: qualifying customers who meet our lending and affordability criteria can borrow against a portion of their Sidekick portfolio to access cash without selling their investments.

- All in one place: simplify your financial life with your borrowing and investment in one app.

- A forward-looking approach for the modern consumer: traditional banks often only consider property as an asset to lend against. But the world has changed and so have the assets we’re owning. We’re building a modern lender for today’s changing world.

Please remember, investing should be viewed as longer term. Your capital is at risk — the value of investments can go up and down, and you may get back less than you put in.

References:

[1] https://www.chase.com/personal/investments/learning-and-insights/article/tmt-february-eighteen-twenty-two